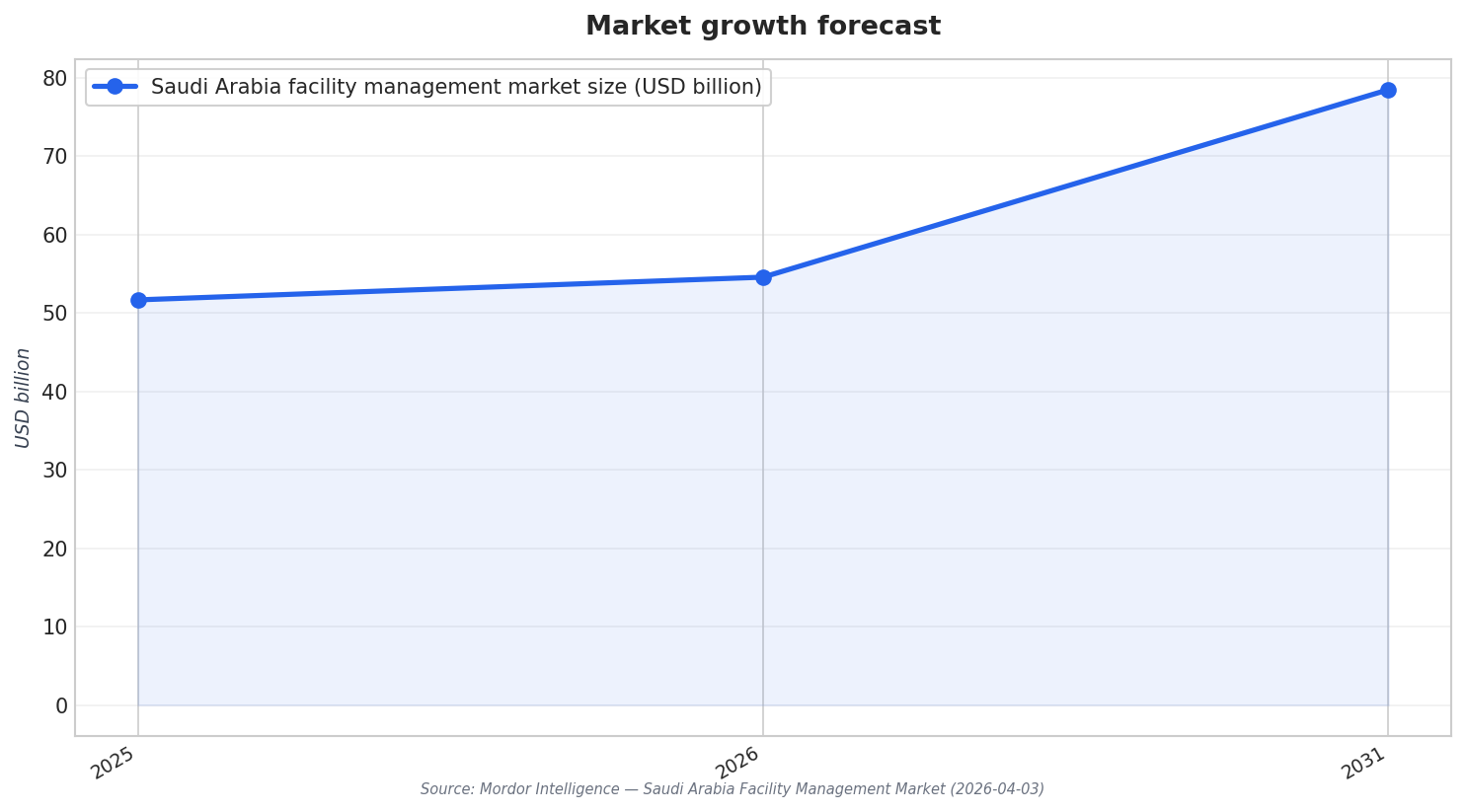

For stadium operators, sports facility management outsourcing in Saudi Arabia is less about copying a template and more about aligning with a market that is already shifting toward specialist providers and integrated contracts. Mordor Intelligence projects the Saudi Arabia facility management market at USD 51.66 billion in 2025 and USD 54.56 billion in 2026, reaching USD 78.46 billion by 2031, with 7.54% CAGR from 2026 to 2031. In that same view of the market, outsourced delivery accounted for 59.36% of market size in 2025 and is projected to grow at an 8.34% CAGR to 2031. That matters for stadiums because it signals mature buyer behavior: procurement expects measurable performance, consolidated governance, and providers that can scale across hard, soft, and sustainability services.

Start your market-entry plan by defining the service mix you will buy, then map it to what the Saudi market already buys at scale. In Mordor’s segmentation, hard services held 54.59% market share in 2025, while soft services are forecast to grow at 8.12% CAGR through 2031. For operators, that suggests first priority on uptime-critical systems and compliance tasks, then building predictable soft-service delivery that can expand with event calendars. The backdrop is a wider pipeline of lifecycle-oriented contracting. Mordor notes mega-projects valued at more than USD 1.1 trillion redefining contracts toward asset uptime, energy optimization, and sustainability reporting, and also cites government privatization of 38 agencies that has opened assets to private operators and increased long-term outsourcing tenders.

How to Structure the First Outsourcing Contract for a Stadium

Contract structure is the market-entry hinge. Credence Research reports outsourced facility management as the leading business model by growth, with a 10.40% CAGR, compared with 8.22% for in-house delivery and 7.67% for sub-contractor hybrid. It also states that fixed-price contracts dominate, followed by cost-plus and performance-based contracts. For stadium operators, this supports a phased approach: start with a clearly scoped fixed-price baseline for day-to-day operations, then attach performance-based add-ons for availability, response time, and event readiness once asset data and service benchmarks stabilize. Credence also frames regional demand differences: the Central Region leads with 38% share, the Western Region holds 32%, and the Eastern Region captures 20%, which can influence staffing, subcontractor depth, and logistics assumptions for multi-venue portfolios.

Digital maintenance is a practical differentiator, but it must be positioned as an operational capability, not marketing. Mordor cites rising IoT adoption embedding predictive maintenance and energy analytics into operations, cutting unplanned downtime by up to 70% and lowering lifecycle costs. The same source also reports field tests where predictive programs reduced maintenance costs by 25–30% and lowered breakdowns by up to 75%. These are not stadium-specific numbers, but they are relevant context when a stadium procurement team asks what “data-driven FM” should deliver. Your entry offering should spell out which assets will be sensorized, how alerts route to work orders, and how energy analytics and reporting will be produced to support integrated governance expectations.

Finally, build compliance and sustainability into your operating model from the start, because it is becoming contractual. Mordor notes mandated compliance with the Mostadam rating system and the Green Building Code, pushing ESG from voluntary practice to obligation. At a regional level, Mordor’s Middle East facility management report expects the market to reach USD 78.25 billion in 2025 and grow at a 13.53% CAGR to reach USD 147.59 billion by 2030, and links growth to outsourcing and integrated service bundles alongside BMS and IoT adoption. For stadium operators, the market-entry checklist is clear: procure integrated capability, contract to measurable outcomes, and operationalize sustainability reporting in the same governance framework as MEP reliability and guest-facing services.

What makes outsourcing a practical entry path for stadium operators in Saudi Arabia?

How should a first stadium FM contract be priced and structured?

Which service areas tend to lead in Saudi facility management demand?

What results are associated with predictive maintenance and IoT in facility management?

How do stadium operators approach sports facility management outsourcing without overbuying?